Linda Price+FollowWhy High Earners Still Feel BrokeEver wonder how a couple making $200K a year can still feel strapped for cash? Turns out, big paychecks don’t always mean financial freedom. Dave Ramsey called out a couple for living large—think $800K house, fancy cars, and a trailer—while juggling debt. The real issue? Spending habits, not the house. Ramsey’s advice: cut back on extras, sell what you don’t need, and tackle debt head-on. It’s a reminder that lifestyle creep can sneak up on anyone, no matter your income. #Business #MoneyTalk #DebtFreeJourney00Share

nkent+FollowStuck in a debt loop? Here’s what Ramsey saysEven with a $75K income, Janet from Boise says her family’s bills feel never-ending—paying late, then facing the same cycle again just a week later. Dave Ramsey didn’t sugarcoat it: he told her to ditch the RV, stop eating out, and get brutally honest about where every dollar goes. His point? It’s not just about making a budget—it’s about sticking to it, together, every single week. Have you ever felt like your paycheck disappears before you even see it? What’s helped you break the cycle? Let’s talk real-life strategies that actually work. #Business #MakeMoney #DebtFreeJourney00Share

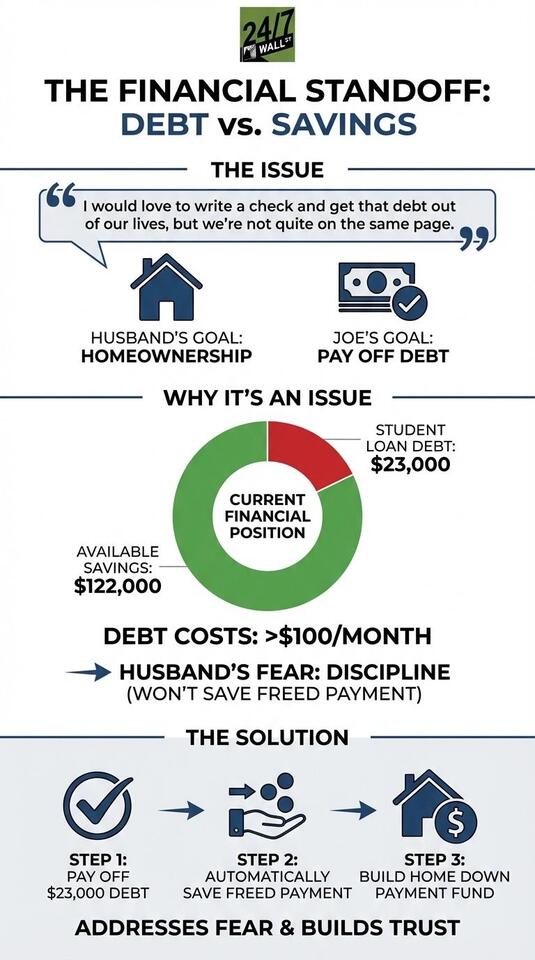

Mrs. Jessica Morgan+FollowShould You Pay Off Debt or Buy a House First?Ever argued with your partner about what to do with your savings? One couple has $122K in the bank but is still paying $100+ a month on student loans. The catch? The husband wants to save for a house first, worried that if they pay off the debt, they’ll just spend the extra cash. The lifehack: set up automatic transfers so those freed-up payments go straight into your house fund. That way, you kill the debt and keep your savings goals on track! #Business #MoneyTalks #DebtFreeJourney00Share

Alexander Black+FollowWould You Buy a Car for Half Your Salary?Imagine leasing a car for three years, then being told you can buy it for $19K—even though you and your spouse only make $40K a year. Sounds like a steal, right? Not so fast. The Ramsey Show hosts say it’s a trap: most Americans are living paycheck to paycheck, and taking on more debt for a car is a fast track to broke. Their advice? Ditch the loan, consider going one-car, and don’t let a “deal” wreck your finances. #Cars #PersonalFinance #DebtFreeJourney00Share

nkent+FollowSix-figure salary, but still drowning in debt?Earning $100K a year doesn’t guarantee financial freedom—just ask Lance from Ohio. Despite a solid income, he’s buried under $65K in debt, mostly from a new truck and Harley. Even after cutting back, he’s still struggling. Turns out, high earners across the country face the same trap: big paychecks matched by even bigger bills. Surveys show that many six-figure earners live paycheck to paycheck, often without a clear budget. Have you ever felt like your money just disappears? What’s your best tip for keeping spending in check? Let’s talk budgeting strategies that actually work! #Business #MakeMoney #DebtFreeJourney00Share

Benjamin Contreras+FollowHow These Grads Crushed Student Debt FastStudent loans don’t have to haunt you forever! Some grads paid off huge balances in under 10 years—without putting life on pause. Lauren refinanced and side-hustled her way out of $125K, Christopher hustled multiple jobs and beat the interest clock, and NiaChloe planned ahead, worked through college, and prioritized paying debt early. Their stories prove there’s no one-size-fits-all, but creative strategies (and a little hustle) can make a huge difference. #Education #StudentLoans #DebtFreeJourney31Share

Thomas Woods+FollowIs a $600 lump sum payment the same as adding $50 every month to my mortgage?My wife and I were lucky enough to lock in a 3.5% rate during COVID, and I’ve been adding an extra $50 to our principal every month to chip away at the loan. I'm starting to wonder if just making one $600 payment once a year would go the same distance as those twelve $50 payments. It might be a dumb question, but I want to make sure I’m actually being efficient with the extra cash. Does the timing of these principal-only payments really matter for the interest in the long run, or does it all balance out the same? #Homeowners #MortgageTips #FinancialAdvice #PrincipalPayment #DebtFreeJourney 11Share

Linda Price+FollowHow Debt-Free Turned Into Debt-HeavyEver wonder how you can go from living the debt-free dream to juggling 13 credit cards? One retired couple did just that after following Dave Ramsey’s advice, only to slip back into $46,000 of debt. The real kicker? They kept borrowing to pay off old debt, thinking it was the answer. The takeaway: swiping for today can mean stress for tomorrow—budgeting beats borrowing every time, especially on a fixed income. #Business #MoneyTalk #DebtFreeJourney00Share

Samuel Gutierrez+FollowHow Lifestyle Creep Eats Your PaycheckEver feel like your bank account should look better, but somehow you’re always broke? This couple in their 20s looked like they had it all—fancy degrees, good jobs, nice digs—but were secretly drowning in nearly $1 million of debt. Dave Ramsey gave them a reality check: no more takeout, no new gadgets, just beans, rice, and hustle. The real culprit? Lifestyle creep—spending more just because you earn more. Time to check if your spending matches your income, not your dreams! #Business #MoneyTalks #DebtFreeJourney00Share

davenportmeghan+FollowWhy paying off your HELOC beats refinancingEven with a paid-off home and solid income, Josh and his wife in Seattle found themselves stuck after borrowing $105K on a HELOC for home renovations. Despite no mortgage and a healthy paycheck, they’re only making interest payments and feeling frustrated by the lack of progress. The Ramsey Show hosts didn’t mince words: instead of rolling the HELOC into a new mortgage, they urged the couple to cut spending and aggressively pay down the debt. Their advice? Pause extras like vacations and retirement savings until the HELOC is gone. Would you hit pause on your lifestyle to get debt-free faster? #RealEstate #DebtFreeJourney #HELOC00Share